When comparing savings accounts, loans or investment products, the advertised rate can be misleading because it often reflects only the nominal (or stated) interest rate. The Effective Annual Rate (EAR) adjusts for the impact of compounding and reveals the real annual cost of borrowing or return on investing. This article introduces the EAR concept, explains how to calculate it and shows how an EAR calculator helps you make better financial decisions.

Why the Effective Annual Rate Matters

Imagine two investments: one offers a 6 % nominal rate compounded monthly, and the other offers the same 6 % nominal rate but compounds quarterly. Although the nominal rate is identical, monthly compounding yields slightly more interest because it applies the rate more frequently. The EAR quantifies this difference, making it easier to compare options fairly.

Compounding frequency — the number of times interest is added to the principal each year — is the key factor in the EAR calculation. More compounding periods mean the interest you earn (or pay) starts earning its own interest sooner. Therefore, investments and loans with frequent compounding end up with higher effective rates than those with less frequent compounding, even when the nominal rate stays the same.

The EAR Formula

The basic formula for the effective annual rate is: EAR=(1+in)n−1\text{EAR} = \left(1 + \frac{i}{n}\right)^{n} – 1EAR=(1+ni)n−1

where:

- i is the nominal annual interest rate expressed as a decimal (e.g. 0.06 for 6 %).

- n is the number of compounding periods per year.

For continuous compounding, where interest is applied an infinite number of times, the formula becomes ei−1e^{i} – 1ei−1, with eee representing Euler’s number (≈ 2.71828). Continuous compounding yields the highest effective rate for a given nominal rate because interest accrues constantly.

Using an EAR Calculator

While you can compute the EAR manually, a calculator is handy when you need to compare multiple products quickly. Here’s how to use an EAR calculator:

- Enter the nominal rate. Use the annual rate quoted by your bank or lender. If you have a monthly rate, convert it to its annual equivalent before using the calculator.

- Select the compounding frequency. Common options are annual (1), semi‑annual (2), quarterly (4), monthly (12) and daily (365). Some calculators also support continuous compounding.

- Compute the EAR. The calculator applies the formula to produce a percentage that reflects the true annual cost or return. You can repeat the process for several compounding scenarios to see how frequency affects the effective rate.

Example

Suppose you are comparing two savings accounts, both with a 6 % nominal rate. One compounds quarterly and the other monthly. With quarterly compounding (n = 4), the EAR is about 6.1364 %. With monthly compounding (n = 12), the EAR rises to roughly 6.1678 %. Though the difference is only a fraction of a percent, over large principal amounts or many years the impact becomes meaningful.

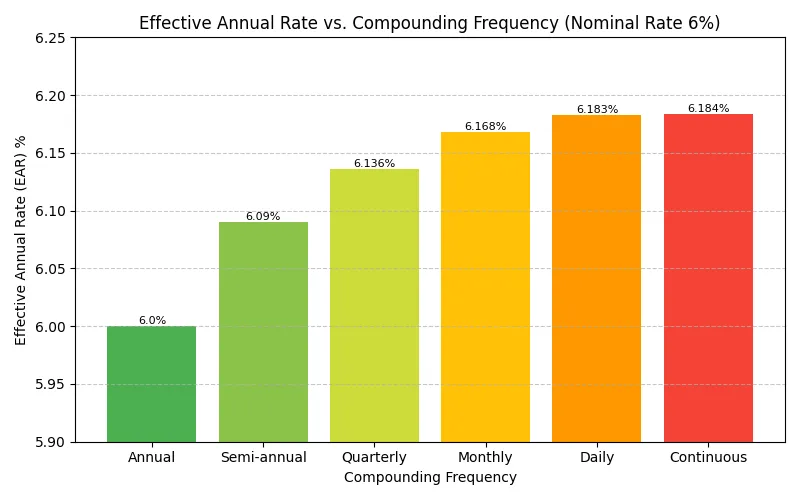

Compounding Frequency and EAR

To illustrate how compounding frequency influences the effective rate, the infographic above compares EAR values for a 6 % nominal rate across various compounding schedules. Notice how the rate climbs from 6 % for annual compounding to about 6.184 % for continuous compounding. Even daily compounding (365 periods) yields nearly the same result as continuous compounding, showing diminishing returns as periods increase.

Limitations to Keep in Mind

- Fixed rate assumption: The EAR formula assumes that the nominal rate remains constant throughout the year. Real‑world rates can fluctuate, especially on variable‑rate loans or investments.

- Fees and taxes: EAR calculations ignore fees, service charges, and taxes that can reduce your actual return or increase the cost of borrowing.

- Inflation: Effective rates do not account for changes in purchasing power. Always consider inflation when evaluating your real return on investment.

Final Thoughts

The effective annual rate is a simple yet powerful metric that demystifies the impact of compounding. Whether you are assessing a loan, comparing credit cards or choosing between savings accounts, the EAR tells you the true annual cost or return. An EAR calculator makes it easy to apply the formula, compare options and make sound financial decisions without needing to crunch numbers by hand.